Early World Cup data made one thing clear: demand was coming. Bookings per property surged across many host markets, and short-term rental operators saw meaningful year-over-year gains. But the latest data tells a more nuanced story. Demand hasn’t ceased; it has concentrated. And for property managers, the difference between capturing that demand and missing it is becoming more visible in the numbers.

Demand Is Rising, But It’s Not Evenly Distributed

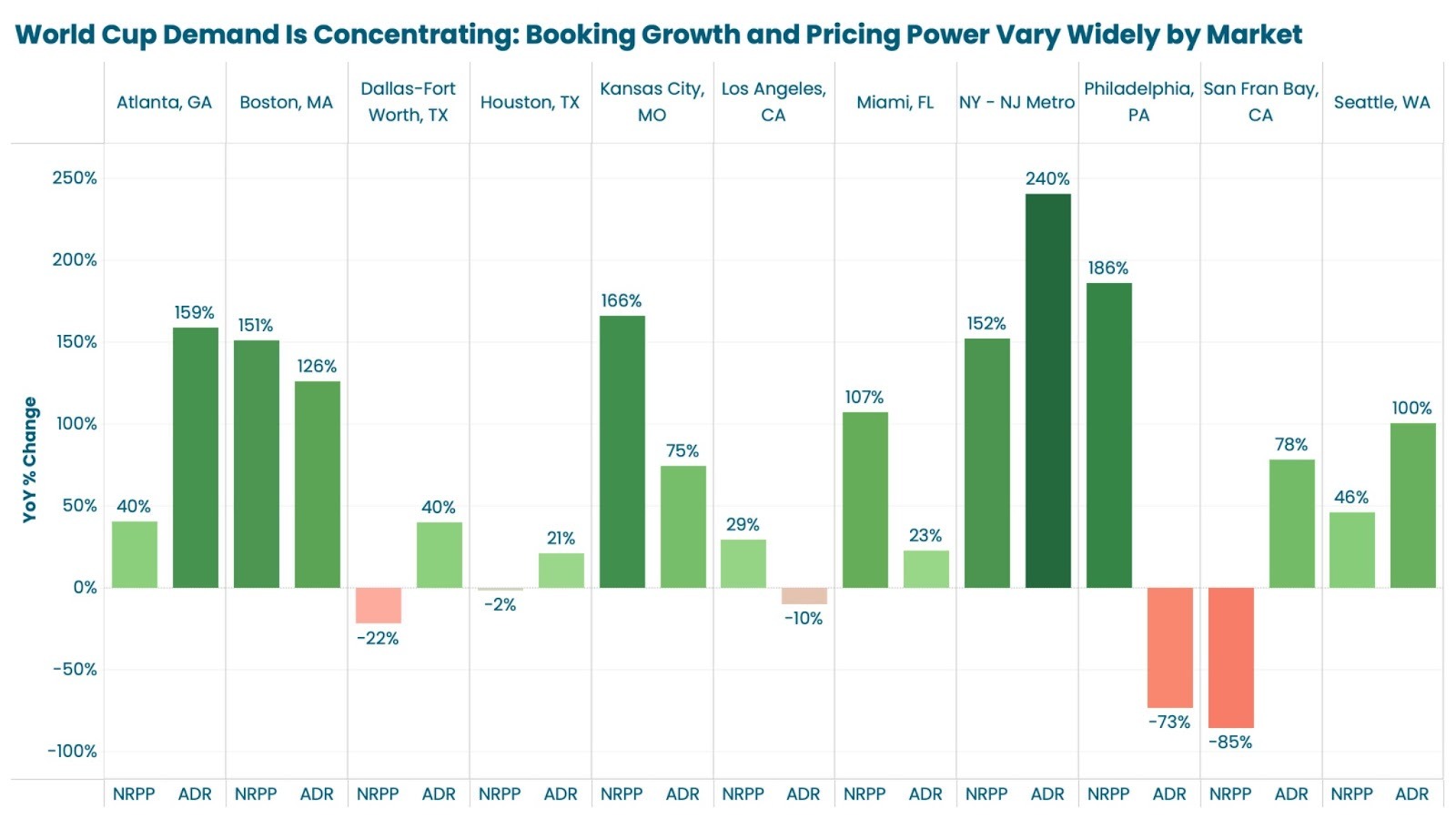

Markets like New York–New Jersey, Philadelphia, and Kansas City are continuing to see strong booking growth, with reservations per property increasing well into triple digits in some cases. At the same time, other markets are already falling behind, with booking declines emerging even as pricing increases.

This divergence matters because it signals a shift in how World Cup demand is being captured. Earlier in the cycle, demand appeared broad. Now, it is becoming selective. Travelers are not just booking, they are choosing the listings and markets that best match how they plan to travel.

And that travel behavior is still highly event-driven:

- Short stays centered around match dates

- Less flexibility on timing

- Higher willingness to pay per night

Pricing Power Is Real, But It’s Not Enough

Across nearly every market, average daily rates are rising. In some cities, ADR is up 50–80% year over year. These higher rates are not always translating into stronger performance, though.

In multiple markets, rising ADR is paired with:

- Declining occupancy

- Shortening lengths of stay

- Flat or negative booking growth

This creates a critical insight for property managers: Raising prices without adapting to shorter, more targeted demand is pushing bookings elsewhere. However, pricing alone cannot compensate for misaligned stay requirements.

The Real Divide: Who Is Structurally Ready?

There are three emerging groups:

1. Balanced operators (winning on both rate and volume)

These operators are capturing strong booking growth while maintaining pricing power. They are aligned with short-stay, high-turnover demand and are converting interest into reservations.

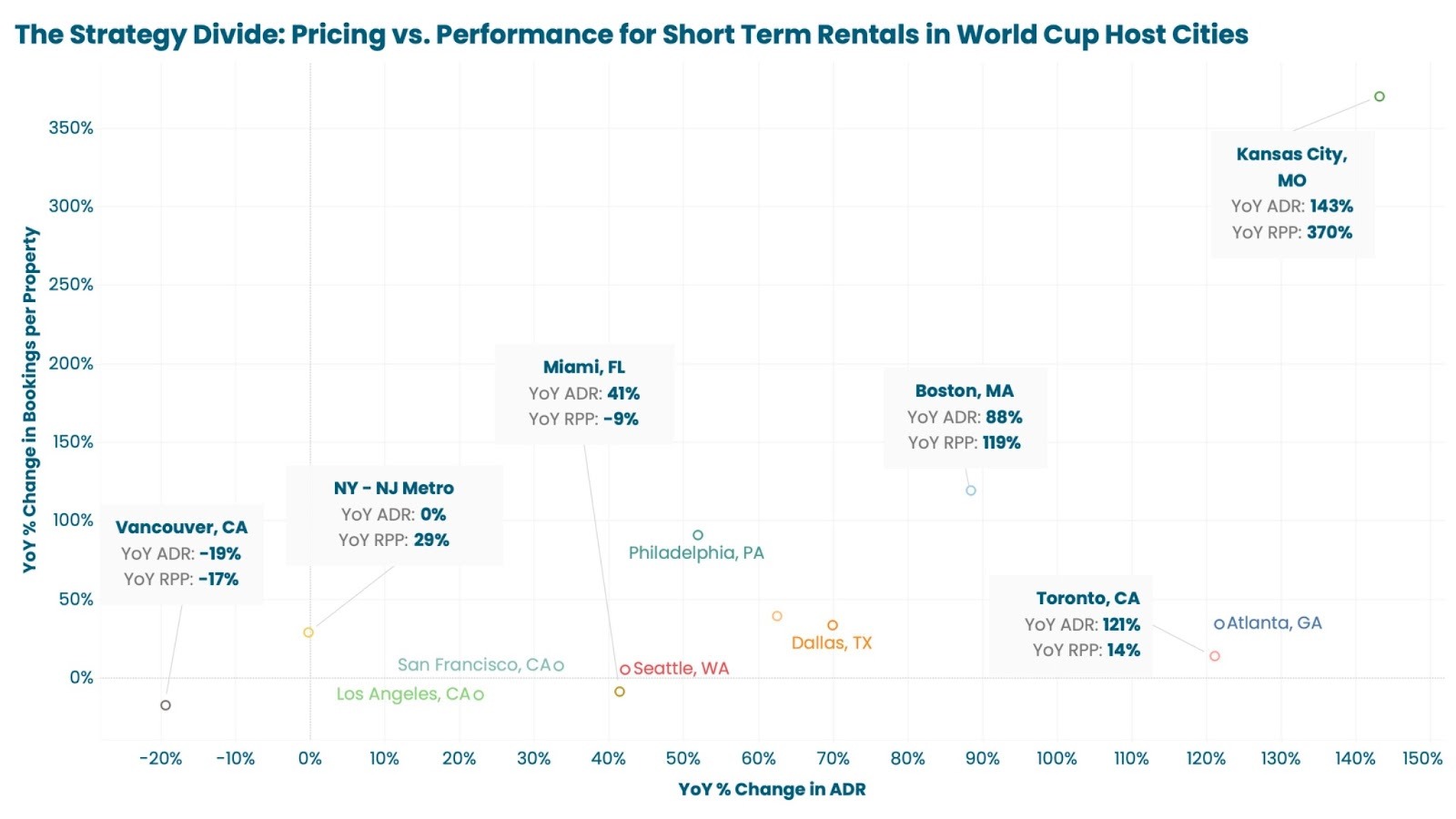

Markets like Kansas City and Greater Boston stand out here. Kansas City, for example, is seeing roughly +370% growth in reservations per property alongside +140%+ ADR growth, while Boston is achieving strong gains across both bookings and pricing. These are markets where strategy and demand are working together.

2. Rate-led operators (pricing up, but losing bookings)

These operators are increasing nightly rates but seeing weaker booking performance. In many cases, rigid length-of-stay rules or inflexible availability are limiting their ability to capture demand.

Toronto is a clear example, with ADR up over +120%, but reservations per property growing only marginally. Miami also fits this pattern, with solid ADR growth but declining bookings per property, indicating that higher prices alone are not translating into stronger performance.

3. Misaligned operators (losing both)

In some markets, both bookings and occupancy are declining despite elevated demand overall. These operators are structurally out of sync with how travelers are booking.

Vancouver stands out here, with declines in both bookings and pricing in the latest data, signaling weak alignment with World Cup demand.

What This Means for Property Managers

Bookings are still happening, but the window to capture them is shrinking.

With the event quickly approaching, the demand curve is shifting again. The early wave of long-lead bookings has already materialized, but a meaningful portion of World Cup demand will come in closer to arrival, driven by:

- Finalized travel plans

- Team progression and match outcomes

- Displaced travelers from sold-out hotels or inflexible listings

This next phase of demand will be faster, more targeted, and less forgiving. The opportunity is still there, but capturing it now requires speed and flexibility.

To compete effectively in this shorter booking window:

- Open up short-stay availability immediately

Many remaining bookings will be 1–3 nights, tied to specific matches. Restrictive minimum stays will block these reservations. - Monitor pricing daily, not weekly

Demand is compressing around specific dates. Adjust rates dynamically based on pickup, not static pricing set weeks in advance. - Fill gaps, not just peak nights

Look for orphan nights between existing bookings and actively price to fill them. Late-stage demand is highly date-specific. - Accept shorter, higher-value bookings

Waiting for longer stays at this stage is risky. A two-night booking at a premium rate is often the highest-yield outcome. - Optimize listings for immediacy

Highlight proximity to venues, ease of check-in, parking, and group accommodations. Late bookers prioritize convenience and certainty. - Prepare for rapid turnover

As booking windows shorten, operational readiness becomes critical. Faster cleaning, communication, and check-in processes will directly impact conversion. - Capture displaced demand

As hotels fill and other STRs remain restricted, flexible operators will absorb last-minute travelers.

The World Cup opportunity isn’t gone, but it has changed. Early demand has already been captured in many markets, and what remains is shorter-term, faster-moving, and more selective. Bookings are still happening, but they are coming in closer to arrival and concentrating around specific dates. This is no longer about waiting for demand to build. It’s about being ready to capture what’s left.

The operators who stay flexible, adjust quickly, and align with short-stay, high-intent bookings will continue to win in the final stretch. Those who don’t may find that even in a high-demand event, the remaining opportunity passes them by.