The latest World Cup data reveals a pattern that should get every hotelier’s attention. Rates are rising across nearly every market. But occupancy and length of stay are not keeping pace. This is not a demand story. It’s a demand conversion story. And the gap between the two is where performance will be won or lost.

Pricing Power Is Strong, But It’s Not Translating Cleanly Into Occupancy

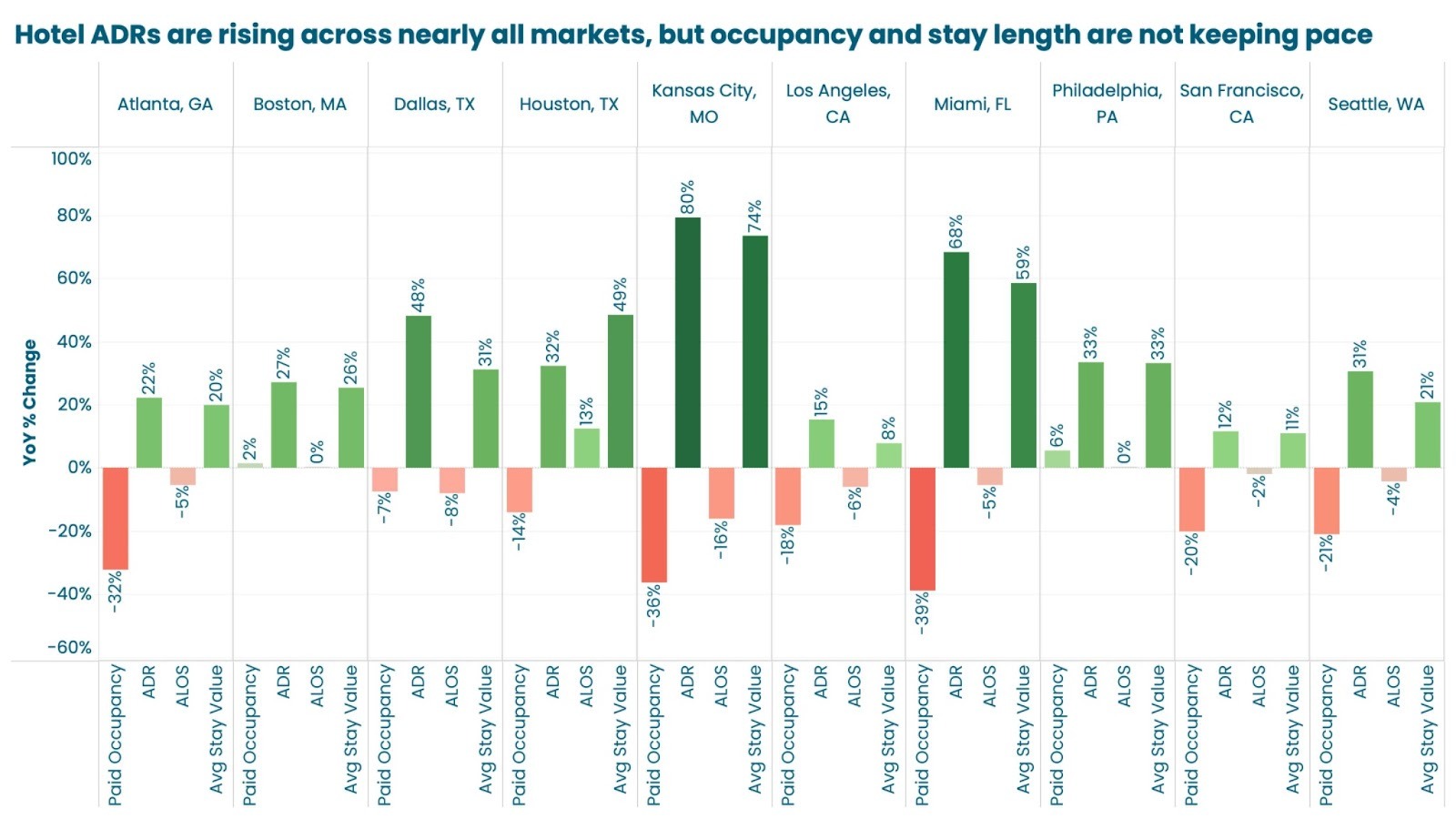

Across host markets, average daily rates are up significantly year over year.

- Kansas City, MO: ADR up 80%

- Miami, FL: ADR up 68%

- Dallas, TX: ADR up 48%

- Houston, TX: ADR up 32%

At first glance, this looks like exactly what hotels would hope for heading into a global event. But the same chart shows something more complicated.

In many of these markets:

- Occupancy is down

- Length of stay is shrinking

- Stay value is being driven primarily by price, not volume

Examples make this clear:

- Kansas City, MO: ADR up ~80%, but occupancy down ~36%

- Miami, FL: ADR up ~68%, occupancy down ~39%

- San Francisco, CA: modest ADR growth, but occupancy down ~20%

Even in stronger-performing markets, occupancy gains are limited relative to pricing growth.

World Cup Demand Is Shorter, Sharper, and Harder to Capture

This pattern reflects a fundamental shift in traveler behavior. World Cup demand is not broad, extended, or flexible. It is concentrated around specific match dates, built around short stays (often 1–3 nights), and less tolerant of rigid pricing or availability. The data shows average length of stay declining across multiple markets, even as pricing increases. This creates a disconnect; Hotels are pricing for peak demand, but travelers are booking for precision. If availability, restrictions, or pricing don’t align with those short windows, bookings don’t convert.

The Risk: Pricing Ahead of Demand

The biggest takeaway from this visual is not that pricing is strong, It’s that pricing may be outpacing realized demand in some markets. Rising ADR without corresponding occupancy growth signals missed booking opportunities, overly aggressive rate positioning, and misalignment with short-stay demand. In practical terms, some hotels are successfully raising rates, but not filling rooms. And in a compressed event like the World Cup, unsold inventory during peak nights is extremely difficult to recover.

Where Hotels Still Have an Advantage

Despite these challenges, hotels remain structurally well-positioned for this type of demand. Short-stay, event-driven travel aligns naturally with 1–2 night availability, operational efficiency for high turnover, and centralized locations near venues. This is an advantage over short-term rentals, many of which are still constrained by minimum stay requirements or less flexible availability. But that advantage only holds if pricing and inventory are aligned with how demand is actually materializing.

What This Means for Hoteliers

With the event approaching, the focus shifts from early positioning to final-stage execution.

To capture remaining demand:

- Align pricing with pickup, not expectations

Strong ADR growth is a signal, but not a guarantee. Monitor booking pace closely and adjust where needed. - Prioritize short-stay availability

Demand is concentrated in narrow windows. Ensure inventory is accessible for 1–2 night stays. - Avoid over-restricting inventory

Length-of-stay rules or rigid availability can block high-value bookings in the final stretch. - Optimize for match-driven demand

Travelers are booking around specific dates, not entire trips. Pricing and availability should reflect that. - Capture late-stage demand

As plans finalize and other lodging options fill, flexible hotels will absorb remaining demand.

The Bottom Line

The World Cup is creating strong pricing power, but it is also exposing where that pricing is not converting into bookings. Higher rates alone are not enough.

The hotels that win in the final stretch will be the ones that:

- Stay responsive to booking pace

- Align availability with short, high-intent stays

- Balance pricing with actual demand, not just projected demand