Early World Cup data made one thing clear: demand was building across host markets. That remains true. However, the latest data reveals a more important question for destination leaders: Is that demand actually being converted into occupied stays? While rates are rising across nearly every market, occupancy trends are far less consistent.

Demand Is Not Translating Evenly Into Occupancy

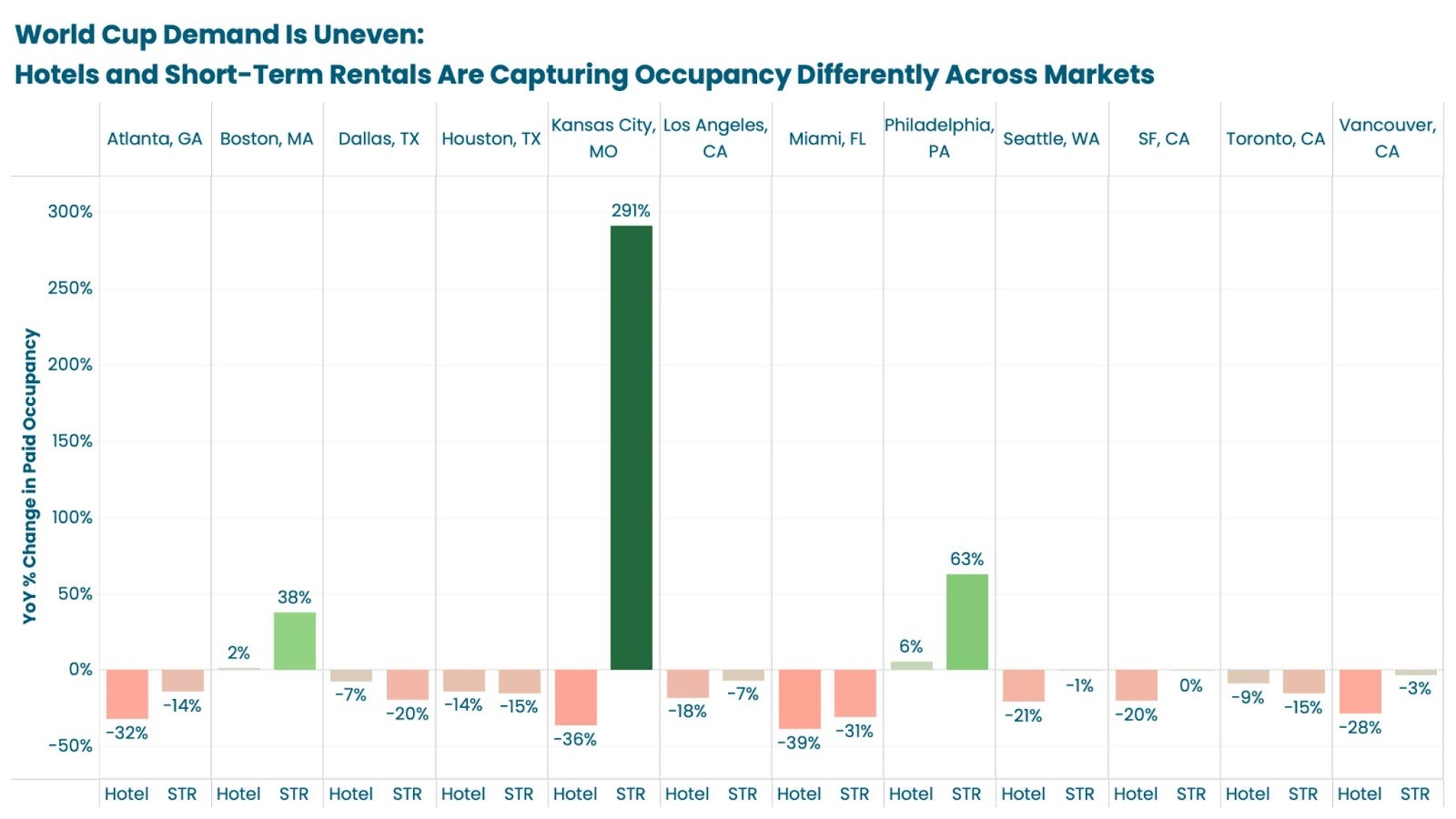

Across host cities, pricing is increasing significantly. But occupancy, the metric that ultimately reflects how many visitors are being accommodated, is moving in different directions depending on the market and segment.

Examples from the latest data highlight this divergence:

- Kansas City: Occupancy down ~36% for hotels, up 291% for STRs

- Boston: Occupancy up 2% for hotels, up 38% for STRs

- San Francisco: Occupancy down 20% for hotels, and consistent YoY for STRs

Demand exists, but it is not being absorbed evenly across destinations.

Shorter Stays Are Increasing Pressure on Capacity

Compounding this dynamic is a consistent shift in traveler behavior:

- The average length of stay is declining across most markets

- Bookings are concentrated around specific match dates

- Travel windows are shorter and less flexible

This means that even when demand is strong, it is:

- More compressed

- More difficult to distribute across the calendar

- Harder to convert into sustained occupancy

From a destination perspective, this creates risk. Shorter stays reduce the total number of nights filled per visitor, requiring higher booking volume to achieve the same occupancy levels.

The Real Risk: Available Inventory Isn’t Always Accessible

The data suggests that in some markets, available lodging supply is not fully aligned with how visitors are booking. Minimum stay requirements can block short bookings, pricing that limits accessibility for certain travelers, and availability gaps around peak match nights are all potential points of friction. The result is a disconnect; Visitors want short, specific stays, but supply is not always structured to accommodate them. When that happens occupancy can suffer, even in high-demand environments.

Demand Is Concentrating Across Markets

The divergence is not just within markets; it is also happening across them. Some destinations are seeing strong booking growth and higher absorption of demand, while others are lagging behind despite similar event exposure. This reflects match scheduling and location of key games, travel accessibility and international demand flows, and differences in lodging flexibility and readiness. The outcome is a fragmented demand landscape where some markets are filling quickly, while others are leaving capacity underutilized.

What This Means for DMOs

For destination leaders, the World Cup is not just a demand opportunity; it is a coordination challenge.

To maximize occupancy and visitor impact:

- Focus on converting demand, not just attracting it

Demand is already present. The priority is ensuring it can be accommodated. - Encourage flexibility across lodging providers

Short-stay demand requires adaptable minimum stay policies and availability. - Promote shoulder nights and extended stays

Encouraging arrivals before and after match days can help smooth occupancy. - Monitor occupancy trends in real time

Identifying gaps early allows for targeted interventions and messaging. - Support balanced pricing across the market

Extreme pricing can limit accessibility and reduce overall visitation. - Distribute demand geographically

Promoting neighborhoods beyond core venues can relieve pressure and improve overall occupancy.

The Bottom Line

World Cup demand is real, but occupancy is not guaranteed. Shorter stays, concentrated booking patterns, and structural friction in the lodging ecosystem are making it harder for destinations to fully absorb demand.

The destinations that succeed will be the ones that align supply with how visitors are actually traveling; ensuring that demand turns into occupied stays, not missed opportunities.