.png)

Destinations attract a diverse mix of travelers, and where visitors choose to stay often reflects how they experience a place. Looking at U.S. performance during the first half of 2026, hotel and direct-booked vacation rental data show distinct travel patterns, particularly around trip planning and length of stay. For destination marketing organizations (DMOs), understanding these differences provides valuable context for campaign timing, visitor forecasting, and destination management.

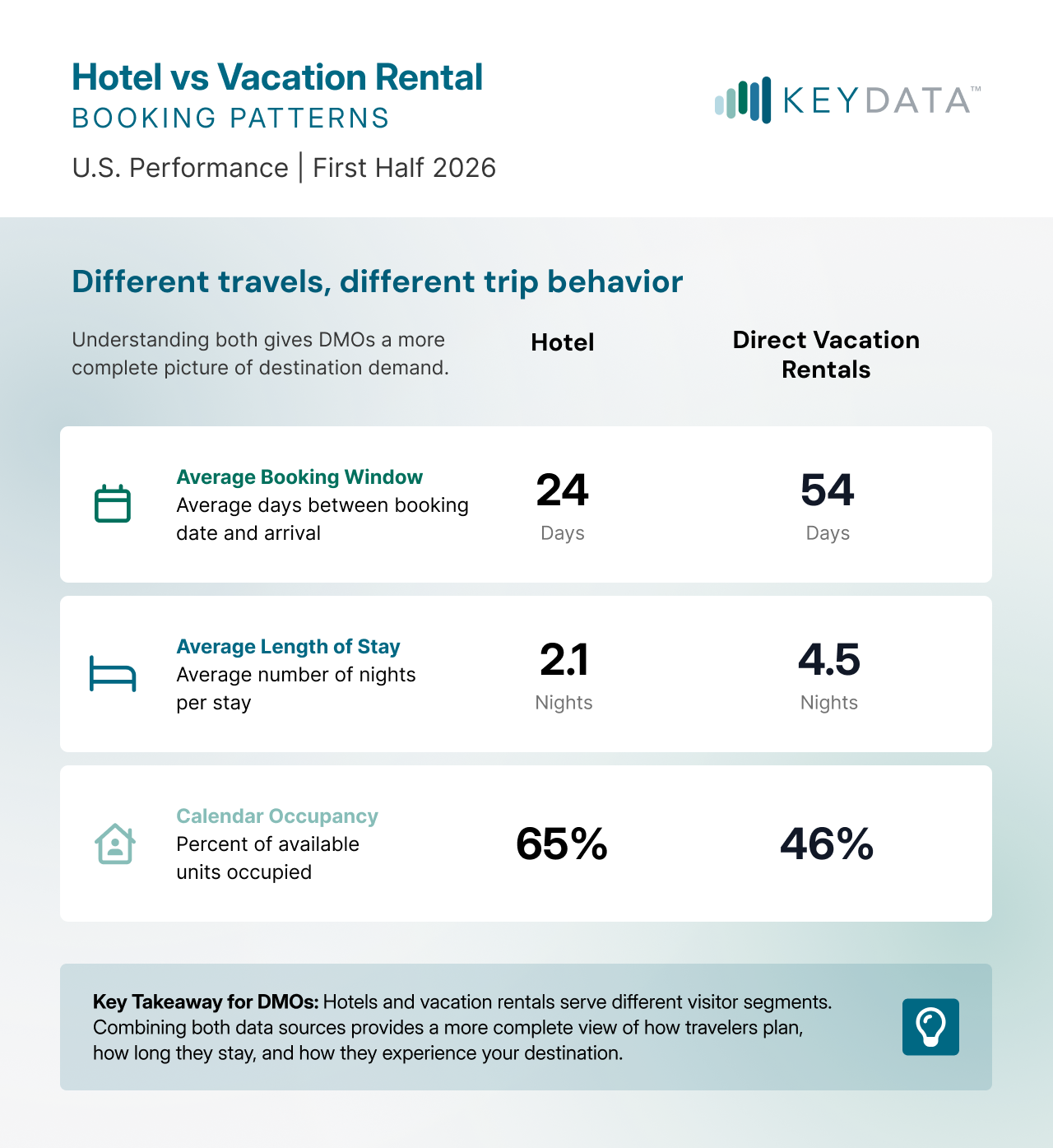

When Travelers Are Booking

The clearest distinction is how far in advance travelers plan their trips. Hotel guests booked an average of 24 days before arrival, while guests booking directly with vacation rental operators planned 54 days ahead. This suggests that many vacation rental stays are part of longer-planned leisure trips, while hotels continue to capture a greater share of shorter-lead bookings, consistent with broader booking trends. For DMOs, this reinforces the importance of maintaining marketing efforts across multiple planning horizons. Campaigns designed to influence vacation rental travelers may need to begin months before arrival, while hotel demand can remain responsive much closer to the travel date.

How Long Guests Are Staying

Length of stay tells a similarly important story. Hotel visitors stayed an average of 2.1 nights, compared with 4.5 nights for direct vacation rental guests. These longer stays can create additional opportunities for visitors to explore neighborhoods, attractions, restaurants, and local businesses throughout the destination. Meanwhile, shorter hotel stays often reflect weekend travel, events, business trips, or stopover visits that contribute to steady visitor volume throughout the year. Together, the two accommodation types illustrate how destinations serve multiple travel styles rather than a single visitor profile.

Hotels vs. Short-Term Rentals

It’s also important to recognize that occupancy metrics represent different operating models. Hotels reported 65% calendar occupancy, while direct vacation rentals averaged 46% calendar occupancy during H1 2026. These figures should not be interpreted as a measure of stronger or weaker demand between sectors. Hotels and vacation rentals have fundamentally different inventory characteristics, booking patterns, and guest behaviors, making direct occupancy comparisons less meaningful than understanding the role each plays within the broader visitor economy.

Viewed together, hotel and vacation rental data provide complementary insights into destination demand. Hotels help illustrate shorter booking cycles and higher-frequency travel, while vacation rentals highlight visitors who plan further ahead and spend more time in the destination. Rather than comparing one accommodation type against the other, combining both perspectives gives DMOs a more complete understanding of how travelers discover, plan, and experience their destination, allowing them to better align marketing, tourism strategy, and stakeholder communications with evolving visitor behavior.