.png)

For decades, hotel revenue management has relied on a simple assumption: if you understand hotel demand well enough, you understand the market. That assumption no longer holds. Today’s travelers do not move through booking curves the way hotel systems expect them to. They commit to destinations earlier, across more lodging options, and with greater flexibility than traditional hotel data can capture. Increasingly, the first place that commitment appears is not in hotel systems at all, it is in short-term rentals.

This shift has created a structural disadvantage for hotels. Hotels are pricing, forecasting, and staffing based on demand signals that arrive after the market has already begun to form. Short-term rental data reveals that gap clearly, and the data shows how costly it has become.

Demand Forms Earlier Than Hotels Can See It

One of the most persistent challenges in hotel revenue management is timing. In many U.S. markets, a large share of hotel bookings finalize within the final two weeks before arrival. As a result, revenue teams are often forced to make pricing decisions well before demand is visible in their own booking curves.

When early hotel pickup appears soft, the conclusion is predictable: demand must be weak. But short-term rental data tells a different story. STRs routinely absorb demand weeks earlier than hotels, particularly for summer leisure travel, peak periods, and event-driven stays. Travelers commit to the destination first, often through rentals, while hotels still appear under-occupied.

This disconnect is not theoretical. It shows up clearly in booking behavior.

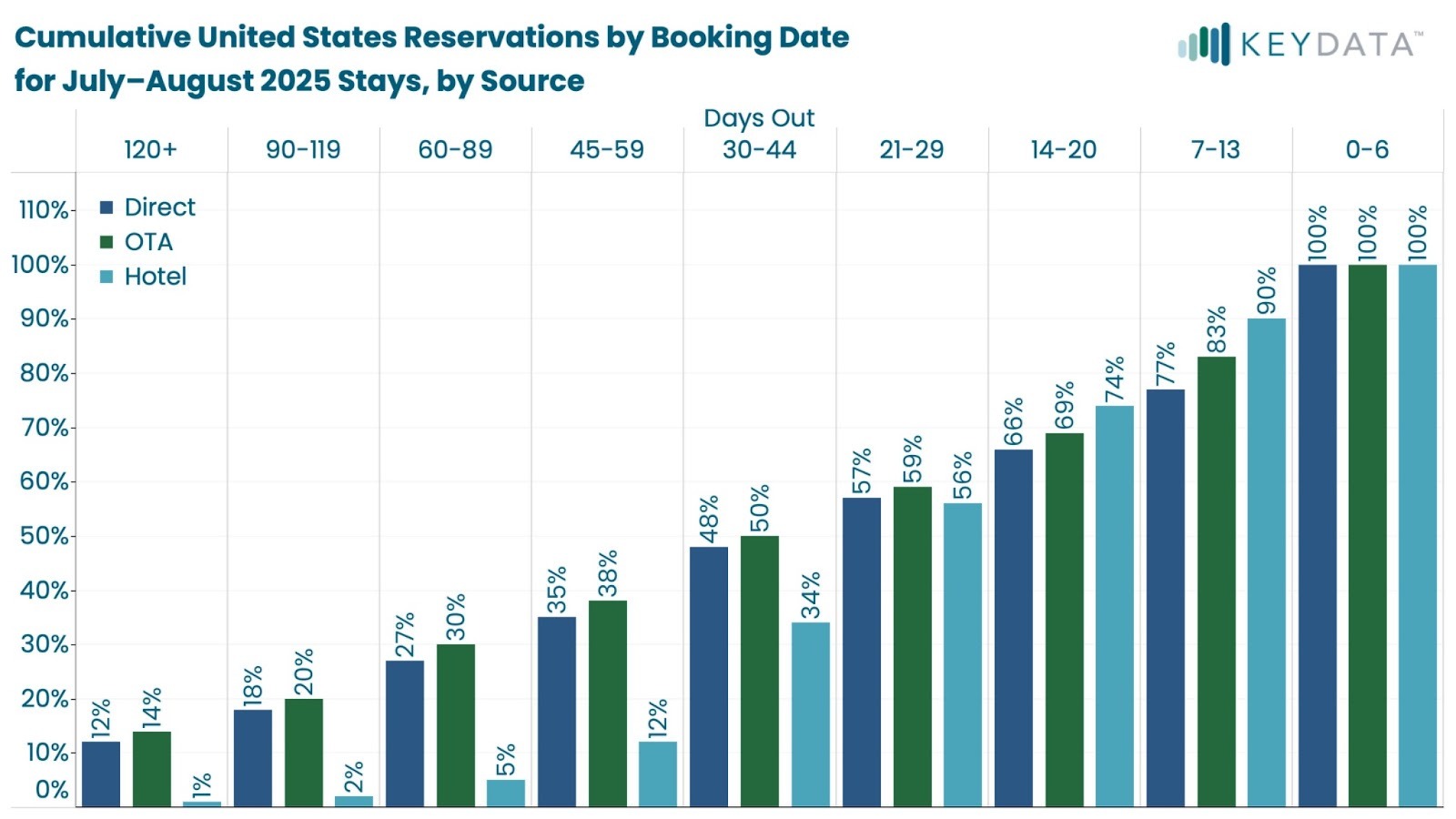

Cumulative Reservations Reveal the Timing Gap

Across July–August 2025 stays, short-term rental bookings reach meaningful penetration far earlier in the booking window than hotel reservations. By 30–44 days out, STRs have already captured a substantial share of total bookings, while hotels remain well below the halfway mark.

Even more telling, hotels do not reach full booking realization until the final days before arrival, long after pricing decisions have already been made. Hotels are pricing before demand is visible, while demand is already committing elsewhere. Without STR data, hotels are not misreading demand. They are simply seeing it too late.

Early Demand Is Higher-Value Demand

The timing gap would matter less if early demand were lower value. The opposite is true.

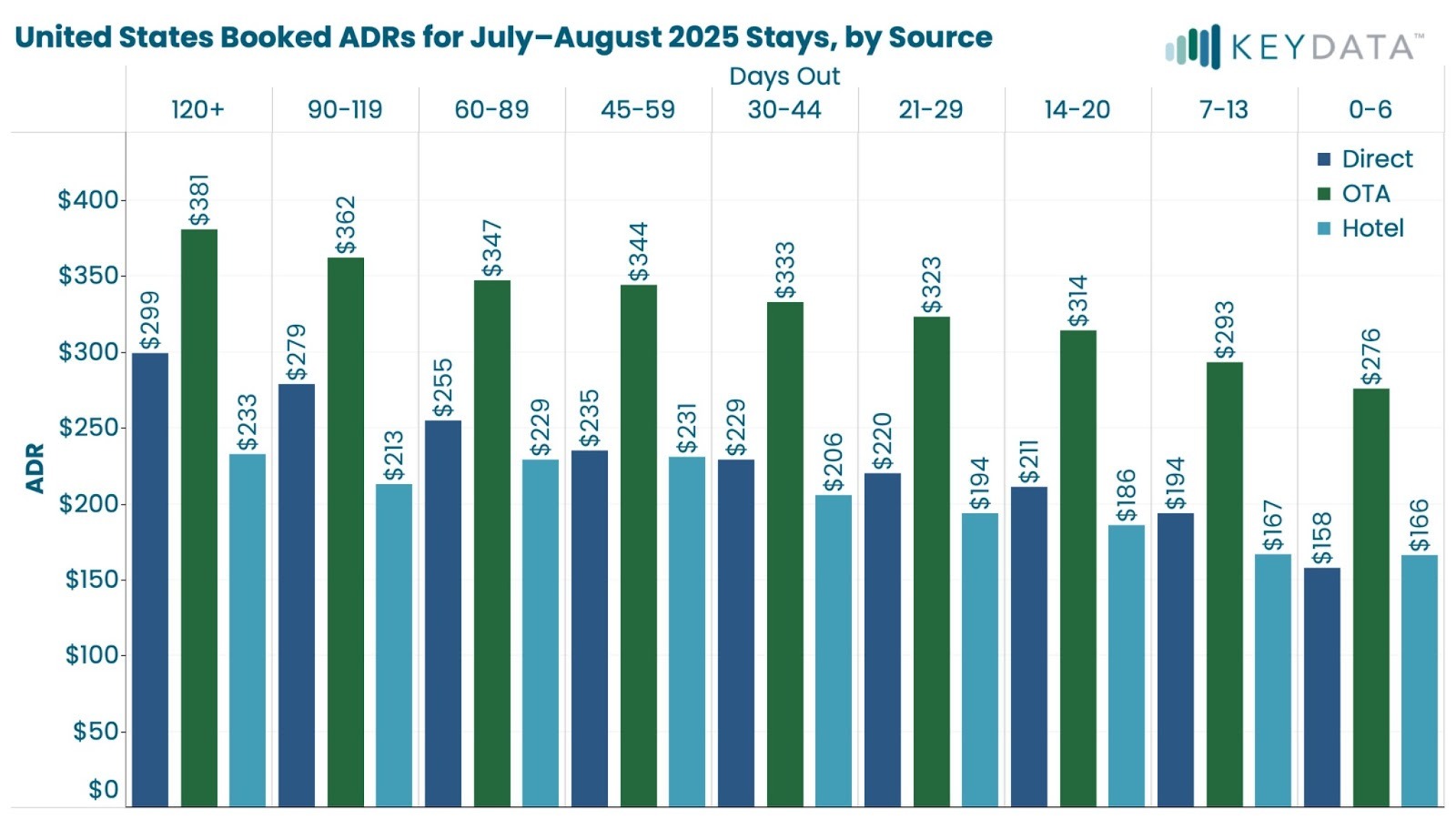

Across every channel, (Direct, OTA, and Hotel) ADR is highest at longer lead times and declines steadily as arrival approaches. Guests who book earlier consistently pay more.

At 120+ days out, booked rates are highest across all sources. As bookings move closer to arrival, ADR declines steadily by the final booking window. Yet hotels often sell early inventory conservatively because their own booking curves have not yet confirmed demand. Rates are held flat, promotions stay live, and inventory is committed at prices that feel safe rather than optimal.

Short-term rental bookings validate demand precisely when ADR potential is highest. When hotels lack that signal, early inventory is systematically underpriced. Once sold, that revenue opportunity cannot be recovered.

Reactive Pricing Compresses Revenue, even in Strong Demand Periods

When hotel pickup finally accelerates, revenue teams respond quickly. Rates rise. Restrictions tighten. Yielding becomes aggressive.

But by then, early bookings are already locked in at lower ADRs, and remaining inventory is limited. Even sharp last-minute price increases apply to too few rooms to materially lift blended ADR.

This is why strong occupancy often coexists with disappointing RevPAR performance. Hotels did not fail to sell rooms; they failed to price them while demand still had leverage.

Short-term rental data changes the sequence. Instead of reacting after pickup shifts, hotels can act on confirmed demand formation; raising rates earlier, protecting inventory longer, and capturing more of the market’s true willingness to pay.

The Hidden Cost of Discounting Into Invisible Demand

The same blind spot also drives unnecessary discounting. When early hotel booking pace lags, promotions are often deployed to “stimulate” demand. Rates are lowered, OTA exposure increases, and rate integrity erodes. But in many of these periods, STR data shows that demand is already present. Travelers have committed to the destination; hotel bookings are simply lagging in timing, not volume.

Without STR visibility, hotels confuse booking lag with demand weakness. The result is margin erosion without incremental occupancy, discounting into demand that would have arrived organically. Short-term rental data gives revenue teams the confidence to hold rates when demand is real but temporarily invisible.

Forecasting Without STR Data Is Structurally Incomplete

The consequences extend well beyond room revenue. Forecasts built solely on hotel booking curves systematically underestimate early demand. Staffing plans lag reality. Marketing teams mistime campaigns. Food and beverage inventory is either rushed or wasted.

When demand is underestimated, service quality suffers and labor costs spike. When weakness is overestimated, promotions dilute margins unnecessarily. Short-term rental data extends the forecast horizon weeks earlier, reducing both upside misses and downside waste. It allows hotels to plan operations around how demand actually forms—not how it appears at the last minute.

A Simple Missed-Revenue Model

The financial impact of late visibility can be quantified using the booking-pace and ADR curves.

For July–August 2025 stays, hotels have booked approximately 34% of their reservations by 30–44 days out, while short-term rentals have already reached 48%. At that same lead time, Direct bookings average $23 higher ADR than hotel bookings.

Those differences do not imply that hotels should price identically to short-term rentals. They do demonstrate that willingness-to-pay is higher earlier in the booking window than hotel pricing reflects.

Using a simple example: if a 100-room hotel books 34 rooms during this early window, and those rooms stay an average of three nights, the missed revenue associated with underpricing is:

34 rooms × $23 × 3 nights = $2,346 for the July–August period alone.

Annualized, that equates to roughly an additional $14,000 per property, without increasing occupancy, simply by pricing earlier with better demand visibility. For a 50-hotel portfolio, that figure exceeds $700,000 annually, purely from timing.

Why Enterprise-Grade STR Data Matters

Not all STR data is created equal. Scraped listings alone cannot reveal true booking pace, realized ADR, or professional operator behavior. What makes STR data actionable for hotels is direct-source, forward-looking booking intelligence, delivered at scale and built for integration into pricing and forecasting workflows.

Key Data’s STR dataset is designed specifically for this purpose; providing earlier, more accurate visibility into demand formation across the full lodging market, not just hotel channels. This is not about tracking competitors. It is about restoring visibility where hotels have lost it.