As the 2025–2026 ski season approaches, new data from Key Data reveals early performance trends across North America’s top mountain destinations. From Vermont to Colorado to California, the latest pacing metrics show how traveler demand, booking behavior, and rates are shaping up for the upcoming winter.

While several destinations are seeing encouraging year-over-year (YoY) growth, others are pacing slightly behind last season—highlighting the importance of rate strategy and dynamic marketing for property managers in ski markets.

Holiday Performance Looks Bright

Adjusted Paid Occupancy = Nights Sold / (Total Nights - Owner Nights - Hold Nights)

Occupancy is pacing consistently ahead of last year, up 6% to 13% year-over-year during key holiday travel windows. The strongest gains are concentrated around Thanksgiving, Christmas, and New Year’s, where traveler demand remains steady across nearly all major ski markets. This growth reflects both renewed traveler confidence and the ongoing appeal of winter leisure travel, particularly among families and groups planning destination ski trips well in advance. For property managers, this upward trajectory presents an ideal opportunity to optimize rate strategies and minimize vacancy during the most lucrative weeks of the season.

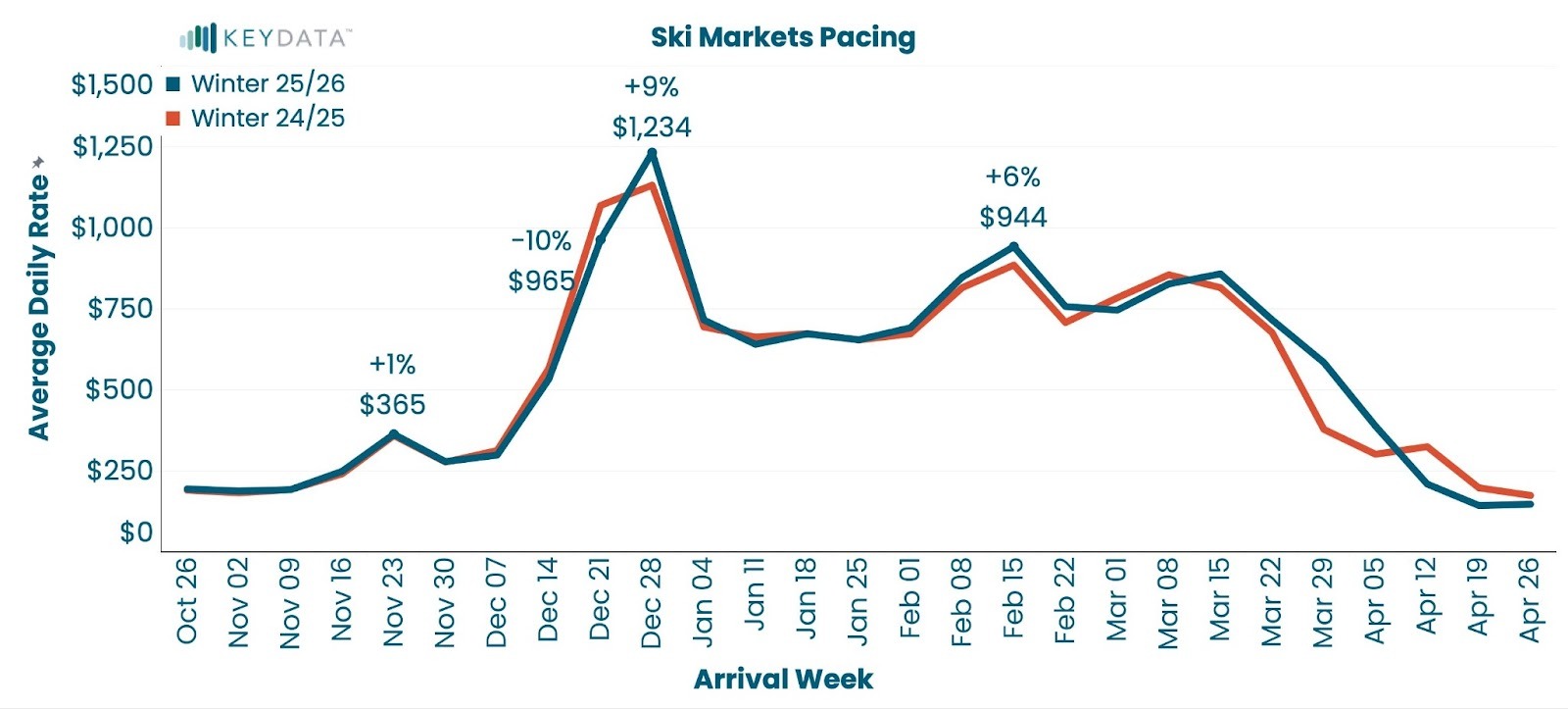

ADR = Total Unit Revenue / Nights Sold

While New Year’s Week (+9% YoY) and Presidents’ Week (+6%) are pacing well ahead of last year, Christmas rates are trending lower (-10%), and Thanksgiving remains steady YoY. With occupancy pacing higher across the entire ski season, property managers have an opportunity to leverage this increased demand by optimizing pricing strategies to capture stronger revenue performance.

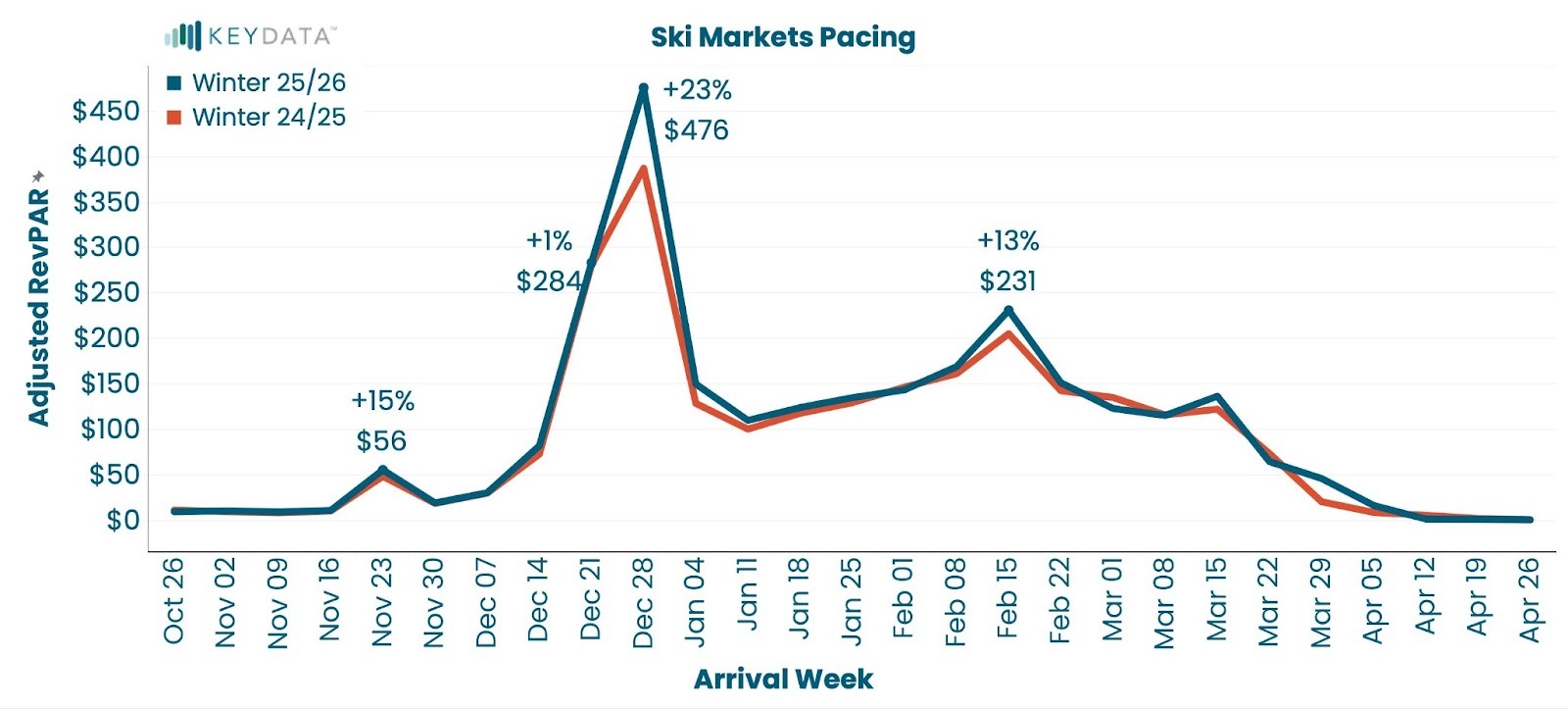

Adjusted RevPAR = Adjusted Paid Occupancy * ADR

Higher occupancy and stronger rates are translating directly into higher overall revenues across ski markets. Thanksgiving week revenues per property are pacing 15% higher than last year, driven by steady demand and early-season rate growth. New Year’s Week stands out as the top performer, with revenues pacing 23% ahead of 2024–2025, reflecting both robust pricing and near-capacity booking levels in many destinations.

Even though Christmas rates are trending lower YoY (-10%), increased occupancy has offset that softness, pushing total Christmas-week revenue +1% higher than last year. This dynamic underscores how balanced revenue strategies, combining flexible pricing with demand-based adjustments, can help property managers maintain or grow profitability even in fluctuating rate environments.

Market Performance: Trends by Destination

1. Increased Occupancy and Increased Rates: Markets with Strong, Balanced Growth

A number of destinations are entering the ski season with a powerful combination of higher occupancy and higher average daily rates, fueling strong revenue momentum. Big Bear Region, CA stands out with occupancy up +27% YoY and ADR climbing +10%, resulting in a +39% surge in RevPAR, the highest of any market. Similarly, Snowmass Village, CO and Mammoth Lakes, CA are performing exceptionally well, with occupancy gains of +26% and +4%, paired with ADR increases of +3% and +24%, respectively. These balanced gains highlight markets where traveler demand and pricing power are both on the rise.

Other markets such as Big Sky / Mountain Village, MT, Steamboat Springs, CO, and Winter Park, CO also show steady improvement in both metrics, translating into RevPAR growth ranging from +9% to +18%. Even in competitive Western regions like Northstar, CA and Summit & Eagle Ski Areas, CO, modest ADR lifts combined with mid-single-digit occupancy gains are driving meaningful revenue growth. Collectively, these markets demonstrate how destinations with healthy advance bookings and steady rate optimization are seeing the most reliable, profitable growth heading into winter.

These destinations exemplify how coordinated rate strategy and growing traveler confidence can amplify overall profitability. Managers in these markets should continue fine-tuning pricing to sustain rate growth while maintaining strong occupancy through peak holiday periods.

2. Increased Occupancy and Decreased Rates: Strong Demand, but Price Pressure Emerging

In several other destinations, occupancy growth is robust, but rates are lagging behind last season’s levels. These markets are benefiting from strong traveler demand, often from drive-to or family-oriented guests, but appear to be encountering price sensitivity or increased competition.

Stowe, VT and Hunter, NY are prime examples, posting remarkable occupancy growth of +43% and +41% YoY, respectively, while ADRs have dipped -15% and -11%. Despite this rate softening, both markets are still producing notable revenue gains (+22% and +26% RevPAR), thanks to the sheer strength of booking activity. Similarly, Purgatory Resort, CO and Okemo Valley, VT show double-digit occupancy improvements (+33% and +22%) that have offset slight ADR declines, resulting in healthy overall revenue pacing.

The outlier in this group, Telluride and Mountain Village, CO, shows occupancy up +8%, but ADR down -10%, leaving RevPAR marginally lower (-3% YoY). These dynamics underscore a key opportunity for property managers: with occupancy momentum on their side, modest rate recalibrations, particularly for shorter lead times, could lift total revenue performance without dampening demand.

3. Decreased Occupancy and Increased Rates: Revenue Resilience Despite Softer Demand

Some of the most interesting dynamics this season are occurring in markets where occupancy is pacing below last year, yet average daily rates continue to climb. This trend suggests that while traveler volume has eased slightly, guests who are booking are opting for higher-end properties and longer, more premium stays; a signal of continued consumer confidence among higher-spend segments.

Sun Valley, ID and Killington, VT lead this category with extraordinary rate growth (+48% and +47%, respectively), more than offsetting occupancy dips (-15% and -21%) to deliver RevPAR gains of roughly +25–26%. These results highlight the value of strong brand positioning and loyalty among repeat skiers, even in smaller markets.

Aspen, CO and Jackson Hole, WY show similar patterns on a smaller scale, each posting moderate occupancy declines (-1% and -3%) but maintaining ADR increases of +14% and +7%, producing overall revenue growth of +6–16%. In contrast, Heavenly, CA and Crested Butte, CO have struggled to convert their rate increases (+16% and +15%) into revenue growth due to steeper occupancy drops (-21% in both cases), while Taos, NM faces the sharpest challenge with occupancy down -26% despite a +12% ADR gain.

The takeaway here: maintaining rate integrity in softening markets can still yield revenue stability, but success depends on careful pacing management, value packaging, and ensuring rate premiums align with the property mix and guest experience.

4. Decreased Occupancy and Decreased Rates: Soft Spots and Recovery Opportunities

A smaller subset of markets are currently pacing behind last season across both occupancy and rates, indicating lingering softness in traveler demand and competitive pricing environments. Park City Area, UT illustrates this trend, with occupancy down -6% YoY and ADR -9%, leading to a RevPAR decline of roughly -15%.

While this dual decline presents a short-term challenge, it also signals room for recovery. With the right blend of last-minute offers, targeted marketing, and short-stay flexibility, these markets could regain lost ground as the season progresses. Given the historically late booking surges seen in Park City and similar drive-accessible resorts, there’s still meaningful upside potential heading into the core winter months.

Takeaways

The 2025–2026 ski season is shaping up as a diverse but promising landscape for property managers. Markets with both rate and occupancy growth are poised for exceptional performance, while those with rate softening can still achieve revenue gains by capitalizing on high demand. Even in markets experiencing slower bookings, strong pricing strategies and late-season marketing could narrow pacing gaps.

Across all destinations, the common thread is clear: traveler interest remains robust, and operators that use real-time performance data to balance occupancy growth with pricing precision will be best positioned to outperform as the season unfolds.